The Story of a Cap Table: DoorDash

Seed investors and the company's founders saw their stakes in DoorDash diluted as SoftBank flooded the company with money and as Sequoia held firm.

In September 2013, investor Saar Gur was kicking the tires on a potential investment in food delivery startup Fluc. Gur emailed a friend working at Oren’s Hummus, a popular Silicon Valley Mediterranean restaurant: “I met the Fluc team about potentially investing in their business. They mentioned to me that Oren's is a big restaurant for them, and that you know about the service. Have you spent much time with them?”

Gur received a response that could have earned his firm billions of dollars. Sadly, that email only triggered a sequence of events that netted the firm a position worth hundreds of millions of dollars today.

“Fluc is a company I have used at Oren's,” Oren’s Palo Alto general manager, Mistie Boulton Cohen, wrote in her email reply – an opening line so brutally matter of fact that anyone who has made a reference check should know what’s coming. (Fluc would eventually join a well-populated graveyard of failed food delivery startups.)

She directed Gur’s attention to another food delivery company. “My team loves DoorDash as do many of our customers,” she wrote. “Fluc definitely has better marketing material and technology but DoorDash builds a relationship rather [than] just another delivery company who picks up and delivers without much more than that.”

Gur, whose wife is a restaurateur, was a big believer that food delivery could work with the right team, so he tracked down the DoorDash founders, including now-CEO Tony Xu. DoorDash had recently finished Demo Day at Y Combinator. “Tony is just remarkable,” Gur recalls thinking. “We were finishing each other’s sentences.”

Gur proposed leading the company’s seed round. “My only mistake was I think I could probably have led the entire round,” Gur said. “There was the star power – Keith wants to participate. I introduced them to some angels – Semil Shah, a lot of people.” So, Gur’s venture capital firm, CRV, ended up sharing the round with Khosla Ventures, where Keith Rabois was a partner, and a number of angel investors.

“Initially I want to say I owned about 10% of the company,” Gur recalls. I think they then added a few more people into the note, so I think the final ownership may have been just under 10%.”

Notably, Sequoia Capital’s Alfred Lin, the former chief operating officer at pioneer ecommerce company Zappos, passed on the seed round after meeting with the team. Lin worried that the DoorDash model seemed to be predicated on college kids spending their parents’ money. (All four founders met at Stanford where the business started.) The next year, Lin led the $17.3 million Series A round and took a board seat. The round gave Sequoia about one-fifth of DoorDash’s shares.

This is a story about how you get “Sequoia rich.” It’s a case study in why investing early isn’t enough. And it is proof that, even if you pick the right space and find the exact right company to bet on before anyone else, SoftBank can still end up owning more of the company than you. This is the story of DoorDash’s cap table.

As a general rule, after Sequoia invests, there are always plenty of eager followers. In March 2015, John Doerr – as his venture firm Kleiner Perkins was defending itself in a reputationally scarring trial with his former chief of staff Ellen Pao – announced that he was leading DoorDash’s Series B round, giving the company a rich $595 million valuation.

Later that year, DoorDash approached investors about a potential billion-dollar valuation. By December, Uber was raising money at a $62.5 billion valuation. It was the year everyone’s expectations about what was possible with private unicorn valuations exploded.

But then investors suddenly cooled on food. Rival Postmates CEO Bastian Lehmann, who knows when to just state the obvious, told me in a 2016 interview that their fundraising round was “super, super difficult.”

Similarly, DoorDash lowered its expectations. Sequoia agreed to invest again at a similar price to the Kleiner round. The infusion of capital gave DoorDash a lower share price and a higher post-money valuation. DoorDash raised $127 million at a post-money valuation of roughly $700 million.

At the time, it looked like Sequoia was doubling down on a losing investment. In retrospect, it was a genius move. Sequoia had the advantage of being an early investor in Chinese delivery company Meituan. The firm’s partners knew that if someone could make the food delivery model work in the United States, there was a lot of money to be made, so it invested when everyone else was getting nervous.

The round certainly established that Sequoia is not a cuddly investor. Here you have the company’s main partner investing on the cheap when a young founder wants to solidify his unicorn status.

Of course, it would have been better for Sequoia if DoorDash didn’t need the money at all. And this is an essential point: these costly fundraising rounds dilute early investors and the company’s founders. By investing a bunch of money in DoorDash, Sequoia diluted its own early investment while buying that ownership percentage back with new money. That’s the reality of the food delivery business as we would soon see.

DoorDash, hungry for yet more money, went to the most logical place: the $100 billion SoftBank Vision Fund. DoorDash started negotiations with SoftBank’s Jeffrey Housenbold only to learn that SoftBank was going to make a massive, complicated investment in food delivery rival Uber. The Uber round closed and still DoorDash didn’t have a deal. DoorDash became more and more worried about its depleting bank account.

Finally, Housenbold convinced Masa that food wouldn’t be a winner-take-all market. And, in March 2018, SoftBank led a $535 million round that valued DoorDash at $1.4 billion. Xu got his unicorn status but at the cost of heavy dilution.

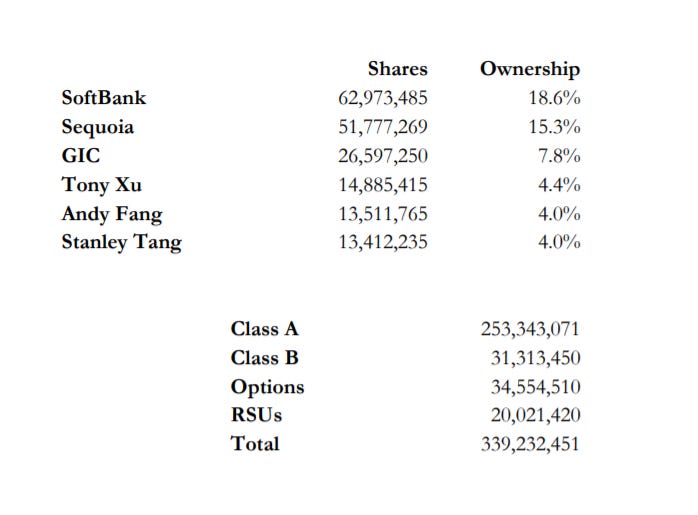

Jeremy Kranz at GIC and Sequoia participated in the mega round that would permanently alter the company’s ownership structure. The deal would help make SoftBank the biggest shareholder in DoorDash, even though Sequoia had invested in the company years earlier and participated in every round thereafter. GIC is now the third largest shareholder.

After that, the money started flowing in. DoorDash’s business model looked more secure and late stage investors piled in. DST and Coatue led a $250 million investment at $4 billion in 2018. The company was recently valued at $16 billion in a round led by Durable Capital Partners, which was joined by Fidelity and T. Rowe Price. DoorDash has filed to go public and is expected to begin trading by the end of the year.

Today, Gur owns far less of the company than he once did. He estimates he has a 3% stake in DoorDash. Gur’s firm, CRV, invested about $10 million in the company altogether, exercising its pro rata rights as long as it could afford.

It should go without saying that Gur is ecstatic to own as much as he does in a company that he believes could be the next Amazon. And many early investors would prefer to be judged on their return on money invested, not ownership stake.

Today, Gur operates a larger fund so he could buy more shares of promising portfolio companies along the way. He said his firm is still the largest shareholder in buzzy cloud collaboration company Airtable thanks to this more aggressive strategy.

In the late 2010s, late stage firms were able to buy up a huge percentage of cash-intensive companies as early stage investors were ill-equipped to defend their positions. DoorDash raised more than $2 billion as a private company. “If we bought 10% and maintained our pro-rata...we would have invested $240 million in the company (almost the size of our fund),” Gur explained in an email.

Regarding Sequoia’s persistent investing, Gur says, “I'd love to know total dollars into the company – it's not an insignificant amount of capital. I just have so much respect for their conviction level.”

I got the answer. A source tells me that altogether Sequoia invested $217 million in DoorDash, exercising the firm’s pro rata rights along the way, leading the Series C, and joining those late stage rounds. Investing in the Series A set them on the path to amass an enormous stake in the company, but it wouldn’t have been enough. Khosla Ventures, Kleiner Perkins and other early funds are now minor investors with less than 5% stakes in the company.

Sequoia has a 15.3% stake in DoorDash, accounting for dilution. Even at just a $16 billion valuation, that stake is worth $2.4 billion.

Despite the hard work from Sequoia, SoftBank owns more – though it certainly paid more for its stake. SoftBank owns 18.6% of the company.

The dilutive fundraising rounds hurt DoorDash’s founders. Xu owns 4.4% of the company and his two remaining co-founders own 4% each. Compare that to Airbnb’s co-founders. CEO Brian Chesky owns about 12% of his company, while his two co-founders own 11% each. (I tweeted out Airbnb’s cap table last night.)

If you read through DoorDash’s IPO prospectus, CRV doesn’t even make the footnotes. Oren’s Hummus got a couple mentions though.

“Fighting for the underdog is part of who I am and what we stand for as a company,” Xu writes in his investor letter. He recalls speaking to “countless merchants since DoorDash’s founding in 2013,” including, “a Mom and Pop store like Oren’s Hummus.”